How to set up a money system you can ignore (and it still works)

A good money system should not need you to become a different person.

It should not rely on you checking five apps every day, remembering every bill date, or suddenly enjoying spreadsheets. For many people with ADHD, that kind of system works for about four days, then disappears under normal life.

The better goal is this: build a money system for ADHD that keeps going even when you are tired, distracted, busy, ashamed, overwhelmed, or avoiding your bank app.

Instead of asking, “How do I stay on top of everything?” the better question is:

How much can I make automatic, visible, and difficult to accidentally break?

Why money systems often fail with ADHD

Across NeuroMoney, we often come back to the same point: money problems are rarely just about money.

Remembering dates, switching tasks, opening apps when you're behind, making decisions when your brain is tired, planning for future costs that don't feel real, and staying calm enough to look at numbers without shame are all hidden money loads.

That is why we try to approach money differently at NeuroMoney.

An ADHD-friendly money system has a different goal. Most importantly, it should still work on imperfect days, which are almost every day.

That is the kind of system this article is about: not a budget you have to babysit, but a setup that does its job in the background.

More here: Why financial decisions can feel harder with ADHD (https://neuromoney.io/blog-adhd-finances.html)

The aim is boring reliability

A money system has to work across ordinary weeks, messy months, and the parts of the year when motivation drops

That usually means designing around three things:

- Automation: the important stuff happens without daily effort.

- Separation: money has clear jobs, so you are not doing mental maths every time you check your balance.

- Friction: spending mistakes become slightly harder, while good defaults become easier.

This is backed by a wider behavioural idea. In savings research, automatic enrolment changed behaviour because many people stuck with the default rather than actively changing it (Madrian and Shea, 2001).

This is important for people with ADHD because the "default" is whatever happens when life gets busy.

If your default is chaos, chaos wins.

If your default is bills-paid, savings-moved, spending-limited, then the system carries more of the load.

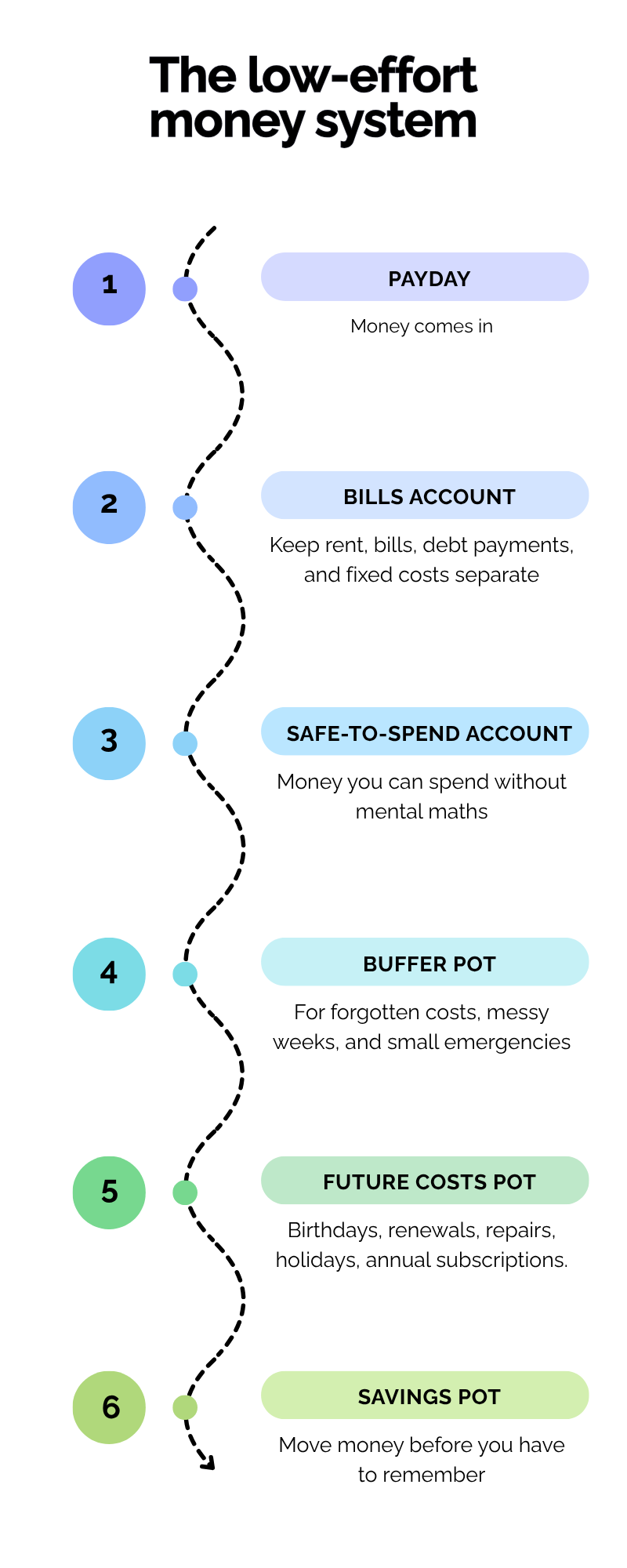

How to create a “safe to ignore” money system

A safe-to-ignore system puts the most important jobs in the right places before life gets messy.

Bills are protected first. Every day spending is separated so you can see what is actually available. Small savings happen automatically. Future costs have somewhere to build up slowly. And if something goes wrong, there is a buffer and a reset point instead of a shame spiral.

Your income comes in, then the system quietly sends money where it needs to go.

You do not need to set all of this up in one day. Start with the part that would reduce the most stress: protecting bills, separating spending money, or creating a small buffer. Once that part is working, add the next piece.

This setup works because each part has one job:

- The bills account protects the essentials.

- The safe-to-spend account gives you one clearer number.

- The buffer pot gives mistakes somewhere to land.

- The future costs pot makes irregular expenses less surprising.

- The savings pot removes the need to remember every month.

A system like this will not make money completely effortless. But it can make the important parts more visible and less dependent on having a perfect week.

What to do when the system breaks

It will break sometimes, and that's okay. You can always make changes to make it work with your unique lifestyle. This is simply an outline that can be tailored to your specific needs.

When things get messy, this is something that might help:

- Protect the essentials: Check rent or mortgage, council tax, energy, food, transport, and debt repayments first. If anything significant has been missed, deal with that before sorting smaller things.

- Stop the leak: Cancel the subscription, freeze the card, move the remaining money, delete the app, or pause the spending trigger. Do the smallest action that stops the situation from getting worse.

- Use the buffer without shame: That is what it is there for. A buffer used for a messy week is still a successful buffer.

- Make one adjustment: If the same problem keeps happening, the system needs to change.

- Restart smaller: Do not rebuild everything at once. Pick one part, test it after the next payday, and adjust from there.

More here: Decision Paralysis as a Financial Cost (The “Frozen Wallet” Effect) (https://neuromoney.io/blog-frozen-wallet.html)

FAQ

What if I do not earn enough to save?

Then the first goal is stability, not savings. Focus on priority bills, reducing avoidable leaks such as subscriptions, and creating even a tiny buffer if possible.

More here: The “Invisible Subscriptions” Trap (And Why Our Brains Struggle) (https://neuromoney.io/blog-invisible-subscriptions.html)

What if I keep raiding my savings?

Make savings harder to access, but not impossible. A separate bank, notice account, or hidden pot can help. You can also rename the pot after the thing it protects, like “rent safety” or “future car repair”, rather than “savings”. If you do need to dip into savings, treat that as information rather than failure. The next step is to either rebuild it slowly or adjust the amount you are trying to save.

Is automation risky?

It can be if the account does not have enough money when payments leave. That is why the base account needs a buffer and a weekly check. Automation works best when paired with visibility.

How often should I check my money?

For many people, once a week is enough for normal maintenance. Daily checking can become stressful, while monthly checking can let problems build. Ten minutes a week is a good middle ground.

Note: This article is educational and is not personalised financial or medical advice.