Why Your ADHD Brain Loves Impulse Spending

(and How to Stop It)

You don’t plan to spend like this. It just happens.

It might be late at night, when your brain is tired, and everything feels louder. Not only that, but it might be after a hard day when you want something to change your mood quickly. Or it might be during a burst of excitement when a “small treat” feels like the right move in the moment… until the next day.

If this sounds familiar, you’re not alone. ADHD is linked with differences in impulse control and reward sensitivity, which can make it harder to pause, weigh up consequences, and delay a decision when something feels good right now (Kurtz et al., 2024; Rodrigues et al., 2021)

This guide is about reducing regret spending without relying on willpower. The aim is not to never buy fun things. The aim is to protect your future self.

(More here: Why financial decisions can feel harder with ADHD)

What impulsive spending can look like with ADHD

For a lot of people, it’s not one big purchase. It’s the repeated “small” ones that add up, especially when they show up in clusters.

Are you buying:

- to fix a feeling (stress, boredom, rejection, exhaustion)

- because you forgot you already own something similar

- because the decision felt urgent in the moment

- late at night when self-control is lower

- because cancelling later feels easier than deciding now (subscriptions are a classic example)

If any of that hits close to home, it can help to treat it as information rather than failure. Your brain is giving you a signal about regulation, energy, and friction. (More here: The “Invisible Subscriptions” Trap (And Why Our Brains Struggle))

Why it happens (without the jargon)

A helpful way to think about this is that your brain isn’t trying to sabotage you. It’s trying to solve a problem quickly.

The problem might be discomfort, boredom, uncertainty, or a sudden wave of excitement. Spending is just a fast tool your brain has learned works.

The “later” part can feel out of reach

In the study above, adults with ADHD reported a lower ability to defer gratification alongside more frequent impulsive buying (Einarsson et al., 2024). That doesn’t mean you can’t plan. It means that in certain moments, “waiting” can feel unusually hard, even if you logically agree that waiting is the better option.

So instead of trying to force yourself to wait through willpower, we design a setup that makes waiting easier.

Positive feelings can trigger spending, not just stress

A lot of advice assumes impulsive spending only happens when you feel low. But research on buying urges in online interactions suggests positive emotion can also play a role in the urge to buy (Lee et al., 2023).

This matters because the fix isn’t “stop enjoying things.” It’s learning how to enjoy things without turning every good feeling into a checkout moment.

Start with the goal you actually want

“Stop spending” is too vague and too harsh. Most people aren’t trying to become minimalists. They’re trying to stop the purchases that cause regret, stress, and financial consequences.

A more realistic goal is:

- fewer purchases you regret

- more time between urge and action

- bills protected, even on messy weeks

- faster recovery when a slip happens

If that feels like your goal, the strategies below are designed around it.

(More here: Decision Paralysis as a Financial Cost (The “Frozen Wallet” Effect))

Practical strategies that work without relying on willpower

The theme you’ll notice is this: we’re not asking you to fight your brain. We’re building “speed bumps” that give you a moment to choose.

- Add a pause you can actually keep

A pause is powerful because it reduces the number of decisions you make at full speed. It also gives emotions time to soften.

Try one of these:

- put it in the basket, close the tab, and set a reminder for tomorrow

- screenshot it and save it to a “later” album

- write the item name in a note titled “things I still want in 48 hours”

If 24 hours feels impossible, make the pause smaller:

- 20 minutes for small purchases

- 24 hours for anything above a set amount (like £30 or £50)

This approach fits what the ADHD study suggests: if delaying gratification is harder, we make the delay easier and more structured (Einarsson et al., 2024).

- Create friction at the point of purchase

Friction is not punishment. It’s a tiny interruption that helps your brain switch from “do it now” to “do I want to do it now?”

Low-effort friction options:

- remove saved card details from shopping sites (this is my favorite)

- turn off one-click buying

- delete shopping apps from your home screen (keep them, just hide them)

- keep your main card out of Apple Pay/Google Pay and use a “spending-only” card instead

- set a daily spending notification so you see the total before it grows

This lines up with how impulse buying is described in consumer research: it’s often fast and emotionally driven, so slowing the moment down matters (Rodrigues et al., 2021).

- Swap “dopamine spending” for “dopamine options”

If you use spending to change your state, you’ll do better with replacement options than with rules.

Make a short “dopamine menu” you can use when the urge hits:

- a 10-minute walk with a podcast

- tea/snack/shower reset

- a quick game you already own

- message someone (or voice note yourself)

- a 5-minute tidy sprint with a timer

This step is about giving your brain another way to get relief or stimulation, especially in moments where emotion is fueling the urge (Lee et al., 2023).

- Make spending a two-step process

If your brain likes “now,” then you need a rule that protects you from “now.” A simple one is:

Step 1: I’m allowed to want this. Step 2: I’m not allowed to buy it at the same time.

How it looks in real life:

- save it to a wish list

- allow purchases only on a planned “spending day”

- write it down and revisit when you’re calm

This can sound small, but it’s one of the easiest ways to reduce regret spending without turning life into constant self-control.

- Use a tiny CBT-style script for urges

One paper on impulse control strategies using a cognitive-behavioral approach describes practical techniques like pausing, reframing, and using structured steps rather than reacting instantly (Ahuja and Gupta, 2022).

A simple script you can use:

- “This urge makes sense. My brain wants relief.”

- “I don’t need to decide right now.”

- “I’ll save it and come back when I’m regulated.”

The point is not to talk yourself out of it with logic. The point is to stop the automatic chain reaction.

- Protect bills first, then make “flex spending” safe

If you’ve ever had a month when one spending spiral made everything else feel unsafe, separating money helps. It turns a vague fear (“I’m ruining everything”) into clear boundaries (“bills are covered; flex is what I can play with”).

A simple setup:

- one account for bills (mostly automated)

- one account or pot for flexible spending

- a weekly transfer into flex so you don’t have to “decide” every day

Some people find that using an ADHD money management tool helps here, not because it fixes impulsivity, but because it reduces decision load and makes separation easier to maintain. The best tool is the one you’ll still use when you’re tired.

A gentle “reset” after an impulsive spend

If you bought something you might regret, the goal is to prevent a spiral.

Try this:

- Pause shame. Say, “That was an ADHD moment, not a moral failing.”

- If a return is possible, set a 10-minute timer to start the return process today.

- If not returnable, name the lesson in one sentence (keep it practical).

- Do one small repair action (cancel one subscription, move £5 back, or set a speed bump).

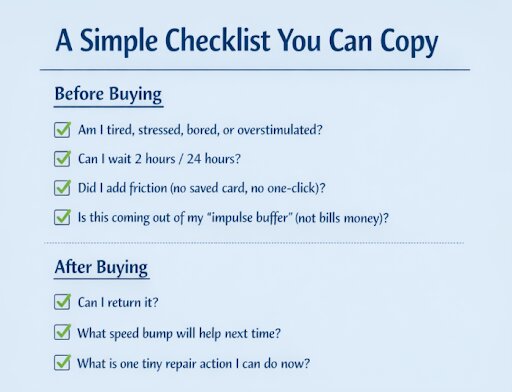

A simple checklist you can use

Ending on a realistic note

If you’ve been carrying shame about this, you can put some of it down. Spending patterns are not a morality test. For many people with ADHD, the gap between intention and action gets wider under stress, excitement, boredom, and overwhelm.

The goal isn’t “never make a mistake.” The goal is a setup that assumes your brain will have off days and protects you anyway. That might mean automating bills, separating spending money, or using an ADHD money management tool that keeps things simple. The best system is the one you can still use when you’re tired.

Note: This article is educational and is not personalised financial or medical advice.